Stock vs Crypto Trading

Stock vs Crypto Trading

Compare & contrast seemingly similar applications

Article Summary :- The crypto trading front-end UX resembles exactly stock trading. However, the UX is not mere how it looks or its appearance , it involves every single direct & indirect touch point the customer has while using the application, including back-end systems & operational risks. Quite a few such UX tasks are done behind the scenes such as Robust Technical architecture, security practices , safety of assets & funds etc. Such parameters are as important, if not more, in ensuring consistent UX. The risks of such parameters are also hidden & cause extreme pain & frustration to customers.Few examples will be downtime during crucial hours, funds stolen, absent customer support etc.

In this article, We will compare & contrast - Stock & Crypto trading and understand how beyond the front end similarities, how much they are dissimilar when it comes to behind the scenes structure.

Introduction

What if you woke - up one day, opened your stock trading app & witnessed in horror that all the stocks you had in your portfolio have vanished. Sounds pretty scary right? However, it rarely happens , if at all. A lot goes on behind the scenes in terms of entity structure & regulation to ensure it. It is still not entirely 100% secure though, as we will see below.

In contrast to stock market which has evolved over a century now , crypto industry is very new & yet to mature. Recently, quite a few users of Coinbase- a centralised crypto exchange with 100BN+ value in market cap, had their tokens stolen. Coinbase is not the only one such story, crypto industry & exchanges are rife with scams & stolen incidents.

In order to understand the reason in detail , we will cover briefly how Stocks & Crypto trading works, entities involved & how are they similar and different.

To start with, quick recap of what it means to be centralised vs decentralised. Centralised entities control your actual funds/securities on your behalf. Through a complex maze of regulations & law enforcement, trust in such entities is generated. They act as custodial intermediaries of sort. Such entities often has one(founder) or group of individuals(Board of Directors) controlling the company directly.

In contrast, Decentralised entities are not controlled by anyone. Trust & Ownership are instead made possible with Smart Contracts(immutable computer codes deployed on blockchains) ,Cryptography & the underlying immutable blockchain technology.

How does your centralised stock trading entities work?

I will continue with the assumption that you understand what “stock” means & represents. How the stock prices are decided & change is beyond the topic of this article. We will primarily look at the components that make online trading of stocks feasible.

Brief Historical Detour

Stock listing & trading existed prior to internet came along.

Hence, it is useful to have a view into stock trading practices prior to wider internet adoption & the impact internet adoption had on the industry.

Earlier, in the 70s, stocks were not commonly bought or even familiar to Retail investors. Institutional investors were the main players. There were few licensed brokers available , with physical stores, that you could visit to buy Mutual Funds or Stocks. As proof of ownership, you would receive a physical certificate copy of the issued Stock/MF. During withdrawal of the MFs/Stocks, you had to present the same physical certificate as proof.

Broker charges were exorbitantly high ( upto 4-5%) . Your trade requests might take days to execute due to unavailability of Sellers of stocks you want buy.

Execution of trade itself was not guaranteed due to such major constraints. The core problem can be represented as “liquidity challenge”.

The Stock seller of, say a company A, had to find the buyer of shares of same company in same quantity in the same city. The buyer & seller order aggregation across cities on a national level did not exist prior to adoption of digital mediums. Before internet, Telephone was indeed adopted.

However, it was still quite cumbersome.

If i wanted to buy , say 100 shares of Reliance, i would go to the Broker to place the order request. Subsequently, the broker would visit the local nearest physical exchange & reach out to other respective brokers looking for sellers of 100 units of shares of Reliance. If not available , the broker would call exchanges in other cities, looking for Sellers & so on.

The physical exchanges ( BSE, NSE, NYSE,NASDAQ) were locations wherein licensed traders & Banks would come together to execute trades.

While today, only few exchanges occupy our mind( BSE,NSE),earlier, since buyers & sellers had to meet physically to execute trades, due to such physical location constraints, quite a few other cities (See image below) had its own exchanges. So, stock trading was quite distributed & decentralised. The local city level exchanges have gradually closed since requirement for city level congregation disappeared over time.

Frequency of buying & selling was quite low. Brokers, in turn, would often work with Banks to execute trades. Hence, the number of middlemen required was also high, making stock trading & investing unattractive for large segments of population. There were other factors contributing to low level of trading & stock investment such as low per capita income, lack of awareness, attractive interest rates on safer Bank deposits & limited number of publicly listed companies on exchanges.

Due to such major constraints, other complicated instruments such as Options did not even exist, even in US. Such instruments needed a broader range of prices to be considered & had complicated maths involved. The rise of computers & digital communication channels in US made Options feasible & it attracted a new wave of mathematicians & CS students/professors into the financial industry fold.

The market crash in 1987 was partially driven by quick adoptions of new complex financial instruments such as Options .This was probably first electronic market crash & the crash speed was very quick . Just as the lack of digital adoption earlier was barrier to participation & reason for slow speed, it also implied that adverse market conditions spread slowly. However, digital adoption had added never seen before speed to the market. Turns out removing friction adds to quick rise & might lead to equally quicker downfall too.

Depository Model

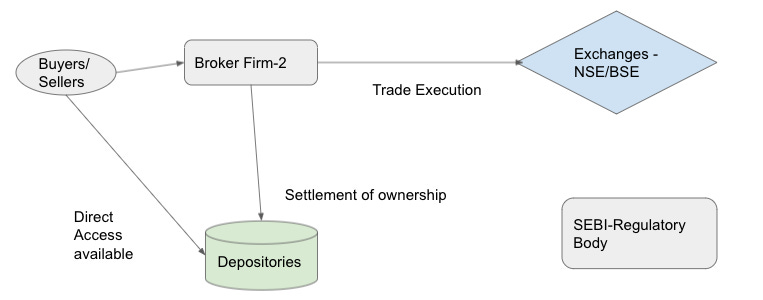

In India , with increasing adoption of internet, Depository model was adopted in 1996. In depository model , an intermediary holds digital certificate on user’s behalf& user can access the ownership certificates with Demat(Dematerialised) accounts.

Demat account adoption in 1996 removed risks with maintaining physical certificate copies with individual owners & associated risks of frauds/forgery/damages encountered with physical copies.

The Indian regulatory body - SEBI instituted it & first depository was established ( NSDL).

Brokerage firms such as Zerodha work with such depositories to open your demat account . The demat account is in your name & you should receive constant communications directly from the depository( Check emails received from NSDL/CDSL with summary of your equity holdings) .

You can also go to the website of such depositories directly to verify your shares/other holdings. Once you start trading, the brokerage firm such as Zerodha helps you maintain digital copy of your ownership with such depositories. The broking entity thus helps aggregate Buyers & sellers, helps execute trades on exchanges( NSE/BSE) & helps you maintain digital certificates with depositories.

All involved entities in the trade, the brokerage firm(Zerodha,Upstox), the exchanges(NSE/BSE) & the depositories(NSDL/CDSL) are regulated by SEBI. In order to ensure ease of use for users, you provide the brokerage firm the right to execute trades on your behalf.

However, technically, the brokerage firm could simply execute a trade without your consent (electronically or otherwise). There have been countless frauds of this sort in the past.

The various entities involved & deliberate distribution of power across depositories & Brokers ensure that no one organisation has extreme control over user’s funds/Stocks & due to redundant channels available for user to interact with & verify its holdings, risks are reduced.

In addition, consumer protection laws add further comfort to retail user participation. Such measure by regulators have played instrumental role in democratising stock investing India over last 2 decades.

While we discussed the stock trading model, few further highlights :-

Stock swapping is still not permitted. If you currently have stocks of company A & wish to buy stocks of company B, then you will need to first sell stocks of Company A & convert it into fiat. Post that you will use the fiat to buy stocks of company B. Crypto token swapping is permitted though in contrast.

Custodian vs Depository model

US has custodian model wherein the Broker itself is liable to hire an external custodian (Citi Bank & JP Morgan for example) ,like a locker room of sort, for storing its client digital form ownership certificates on the name of client/user.

One way to contrast Indian & US approach is difference in power embedded with brokers. In India, users can directly compare its holdings shown in broker account vs within depositories. In US, Broker manage all the contact points with user. The SEBI counterpart in US is SEC & it regulates all involved entities to ensure user’s interests. Each account is further insured upto $500,000 for consumer protection.

Centralised crypto exchanges

Even though decentralisation & ownership is core theme behind crypto, ironically over 80% trading of tokens still happens on centralised crypto exchanges (Binance , Coinbase, FTX etc.) . Familiarity & ease of use of the applications (the UX & trading journey is similar to stock trading) are primary reason behind continued adoption of such exchanges .

But, the high risks entailed is using such centralised exchanges are not known to new users.

Majority of new users are attracted to such exchanges with lure of Token price increase & are unaware of other major risks of theft & scams. Centralised Crypto exchanges have raised venture funds & have started advertising heavily recently. In contrast, the native decentralised crypto applications do not advertise at all. This is one of the major contributing factors behind the gap in actual user numbers ( Early Innovators & Adopters) using native decentralised applications & mere speculators( retail investors). The risks of bubble appear legit at the moment.

Even though, the trading journey on such centralises crypto exchanges seem almost similar to stock trading, the crucial entities behind the scenes - such as regulated depositories(NSDL/CDSL) , brokers(Zerodha) & exchanges(NSE/BSE) that make stock trading relatively safer- are not present in crypto exchanges.

In addition, the alternate decentralised exchanges - crypto native decentralised applications- are still unknown & requires intermediate knowledge of crypto to be able to use it.

Centralised crypto exchanges have some other serious issues - Pathetic customer support, Countless Hacks & Attacks, Outright Scams & thefts,Prone to Ban from Governments, outages during crucial hours, charges of insider trading & price manipulation etc.

There are countless positives though that must be highlighted .

Such exchanges have played instrumental role in making crypto trading more familiar to masses & can be viewed as gateway into more complex & counterintuitive structure of Decentralised applications.Centralised crypto exchanges made tokens accessible to masses, provided liquidity & continues to attract new set of users. You as newcomer will be unlikely to jump on DEX(Decentralised Exchange) /Ownership bandwagon directly without some familiarity first with centralised crypto exchanges first.

Chances are most of exchange names that you have heard are centralised ones- Binance, Coinbase, FTX,Kraken etc. These are the largest exchanges with billions in custody. Technically though, these intermediaries( similar to how brokers work in stock trading) connect with relevant blockchains & own the crypto assets on its users behalf. Such exchanges merely maintain the mapping of crypto assets against each users onboarded in its personal database. The entire token base though belongs to the exchange itself since keys are in control of the exchange.

Trading

When you create an account with a centralised exchange & start trading, it is to be noted that you as “individual user” only exist in internal private database( DB) of the exchange. You as buyers convert your fiat money into crypto tokens. Whenever a trade is executed, only the internal mapping in the DB of exchange shifts between the buyers & the seller. The exchange is in full control of your funds on the blockchain itself.

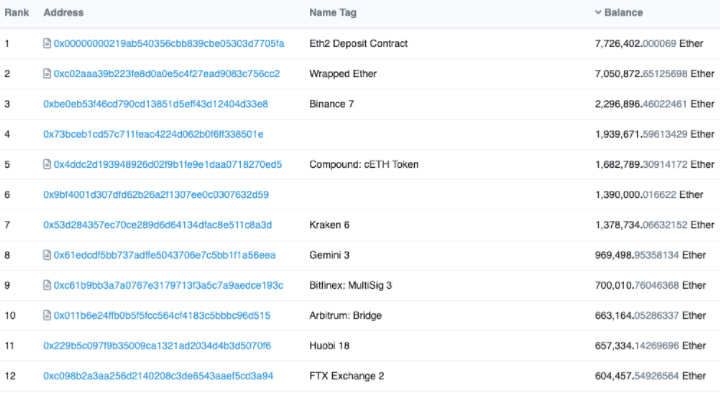

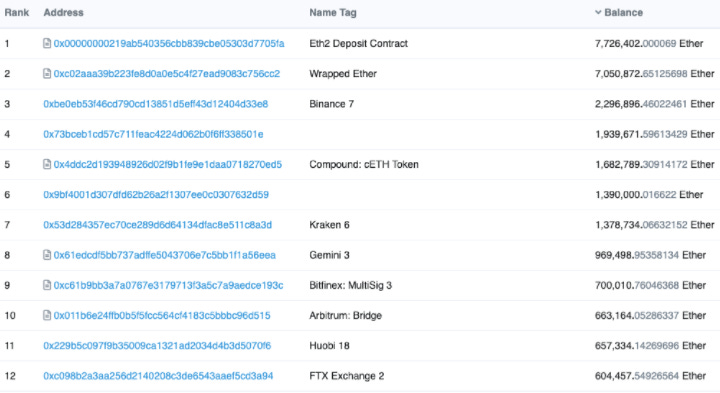

For example, below you can view the biggest accounts on Ethereum blockchain. In the below screen, the major accounts such as Binance,Kraken,Gemini ,Huobi, FTX are all centralised exchanges holding the cumulative balance of its users.

Since, all the trading activity is executed off-chains onto personal DBs of such exchanges between buyers & sellers, the key advantage of speed & convenience is achieved. However, the transparency is completely missing. In absence of regulation(SEBI oversight), explicitly defined accountability,& defined consumer protection laws , the risks to consumers is very high. Such crypto exchanges subsumes the role of broker, depository & exchange in itself- raising the risks of scams.

Centralised crypto exchanges Just imagine, trying to go through legal recourse when no laws are in place, in case of thefts. To make matters worse, quite a few exchanges are quite global in terms of userbase( e.g. Binance) & even legal recourse may not be feasible for you to recover stolen/lost funds.

Anonymity & being able to trade without knowing identity of each user is hallmark of crypto & decentralisation. However, crypto exchanges require you to go through KYC & linking of bank account number for trading. You also have to trust such platforms for ensuring security & safety of your personal sensitive information submitted as part of KYC.

The trade-off involved need to be more well understood by consumers. The hack/stolen funds or lost funds are common phenomena. In crucial hours such say a market crash or rally in specific coins , the applications are not accessible ( website down due to high volume, maintenance). Charges of market manipulation & insider trading are also made of quite a few of such exchanges. Ironically crypto is supposed to be antithesis of extreme centralisation & has somehow produced one such entity in extremely centralised crypto exchanges - exactly what it attempts to replace.

Few highlights

Best Practices :- The best practice would involve moving your crypto assets to such exchanges temporarily when you want to sell the tokens. If a new token is bought, you should move it back to personal wallets. That way you can experience the high liquidity that such exchanges provide & still manage security on our own.

When you want to sell your coins- you must deposit the coins on Exchange’s wallet address. The wallet address is similar to your bank account number for crypto.

This is an actual chain transfer of ownership & can be verified as such. Now when you sell the coins, ownership it still stays with the exchange’s wallet, the buyer information simply gets swapped on your place within the internal DB of the exchange. The new buyer can now withdraw the funds into it’s own wallet with another on-chain transaction.

However, most users leave the funds within exchange’s wallet . The primary reason is unfamiliarity with non-custodial wallet services & cognitive load involved with managing your own funds. The trade-off leads to unaccountable & often relatively new “centralised crypto exchanges” becoming security holes.

One relatively less discussed aspects are linked to topics beyond trading. Such exchanges sometimes do not recognise & list forks to existing tokens. Due to lack of regular audit & missing accountability , charges of market manipulations & insider trading for personal gains have been made in the past. Such power of being able to support one over the another is extremely problematic.

Custodial centralised exchanges are all powerful in crypto space & have not attempted to solve legitimate questions & issue arsing from “conflict of interest” & extreme centralisation.

If the exchange is compromised or owner simply vanishes, you have limited recourse to recoup funds, including legal clause or consumer protection laws. This is not mere theory- in reality such risks have manifested across various various exchanges such as -Mt. Gox, Bitfloor, CoinCheck or more recently Thodex.

In the next article, we will cover Decentralised exchanges & walk through Uniswap to understand the concept .